If you’re still trying to figure out why the Federal Reserve’s profligate money printing is a big deal, perhaps this analysis by Franklin Sanders from his daily commentary email on December 2nd will shed some light on why the Fed’s QE policy is extremely dangerous and is mostly irreversible at this point.

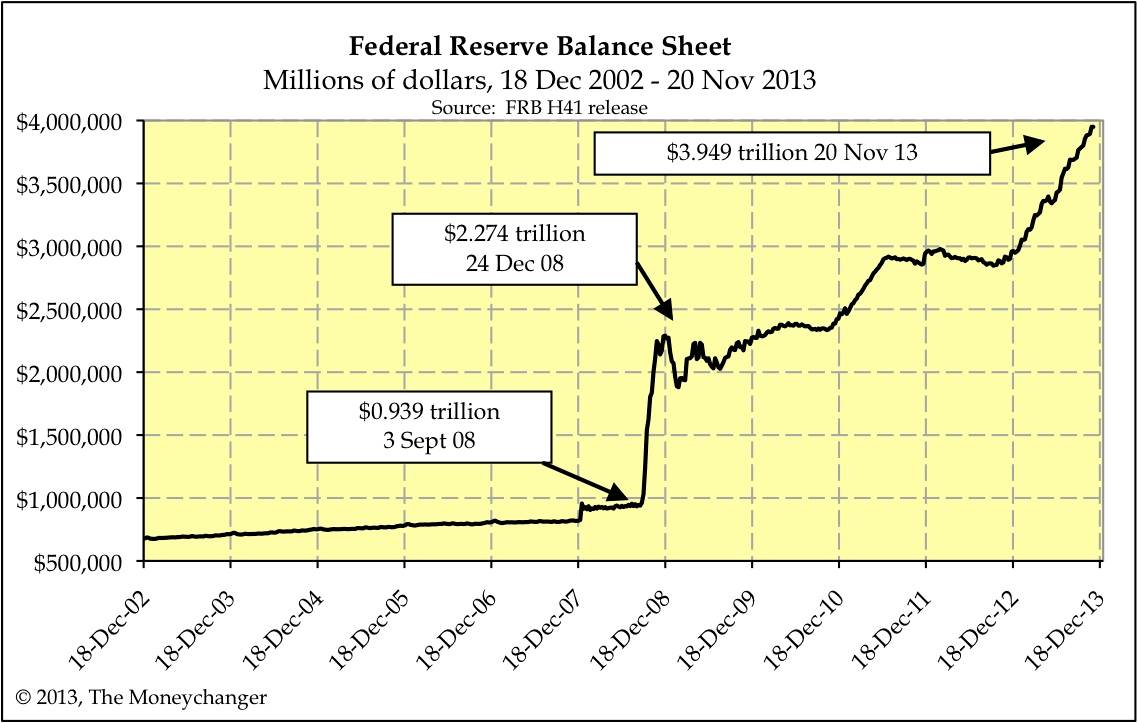

“I read something today that freezes my blood, in Fred Hickey’s Hi Tech letter. “The Fed has now accumulated $2.2 trillion of treasury securities and more than $1.4 trillion of mortgage backed securities, and its balance sheet is nearly $3.9 trillion, FIVE times the level in late 2008, when it began QE1. . . . The Fed now owns nearly half of all treasuries maturing between ten and fifteen years.”

So the Fed has engineered a bubble in US treasuries, lowering interest rates nearly to zero so it made no sense for investors to buy anything but “risk-free” treasuries, except it turns out the Fed owns a vast amount of those treasuries. When interest rates rise, their value declines.

But that’s peanuts and peanut shells, not the big issue. Bernanke has backed the Fed into a very narrow corner. They can’t sell without precipitating a colossal deflation. But even if they could sell, who would buy all those treasuries, especially in a falling market?

The answer comes back: “Nobody.” The bond bubble will deflate very quickly — think “Pin-prick.” And once those interest rates start rising, banks will begin pulling those reserves out of the Federal Reserves’ hands, where they have been sequestered and “sterilized,” say, Oh, roughly $2.5 trillion. And that $2.5 trillion, when the banks loan it into the money supply, will increase, Oh, say, ten-fold.

Blood in the streets inflation does not begin to describe the catastrophe Bernanke has made possible. Better pray it doesn’t come.”